Navigating the Competitive and Crucial Data Encryption Market Landscape

The relentless pace of digital transformation has created an environment where data is both a critical asset and a significant liability, driving the exponential growth of the Data Encryption Market. This market is characterized by intense competition and continuous innovation, fueled by a set of powerful and non-negotiable drivers. The primary catalyst is the escalating frequency, sophistication, and cost of data breaches. A single security incident can result in devastating financial losses, reputational damage, and legal penalties, making proactive data protection a top priority for boards and C-suites.

Furthermore, the proliferation of stringent data privacy regulations worldwide, such as the EU's GDPR and California's CCPA, legally mandates the protection of personal data, with encryption being a specified or strongly recommended control. These regulatory pressures and the high stakes of a data breach are compelling organizations of all sizes to invest heavily in robust encryption solutions. Projections show the Data Encryption Market size growing to USD 40.2 billion by 2032, advancing at a strong 16% CAGR between 2024 and 2032.

The competitive landscape of the market is diverse, featuring a wide array of vendors, from established cybersecurity giants to specialized startups and cloud hyperscalers. Traditional players like Thales, IBM, and Broadcom (through its Symantec and CA Technologies acquisitions) have a strong foothold, particularly in the on-premises and hardware security module (HSM) segments. They compete on the basis of their established brand trust, extensive patent portfolios, and deep relationships with large enterprise customers. In parallel, the market is populated by numerous software-focused vendors offering solutions for disk encryption, database encryption, and file/folder encryption. The cloud has also become a major battleground, with AWS, Microsoft Azure, and Google Cloud Platform embedding powerful and easy-to-use encryption capabilities directly into their services, often making it the default option for their customers.

Market segmentation typically occurs along several lines, including component (software and hardware), deployment model (on-premises and cloud), and enterprise size. The software segment is the larger of the two, encompassing the encryption algorithms and management platforms. The hardware segment, primarily consisting of Hardware Security Modules (HSMs) which securely manage and store cryptographic keys, is a critical and high-margin niche. In terms of deployment, while on-premises solutions remain crucial for organizations with strict control requirements, the cloud-based deployment model is growing at a much faster rate due to its scalability, flexibility, and lower upfront costs. This shift to the cloud is reshaping the market, forcing traditional on-premises vendors to adapt their offerings to hybrid and cloud-native environments to remain competitive.

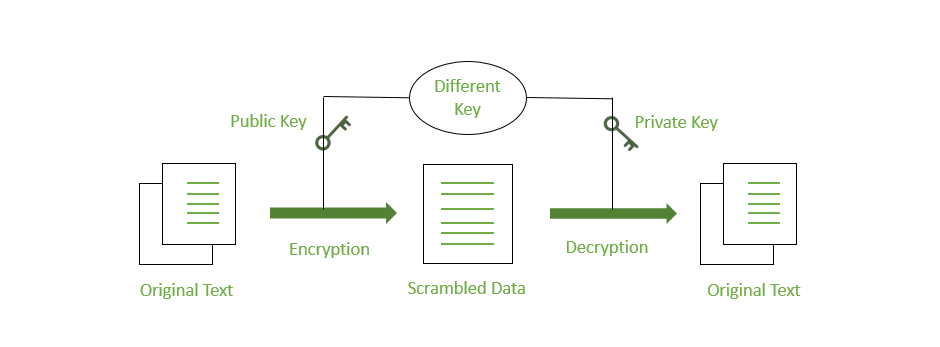

Ultimately, success in this market hinges on a vendor's ability to provide solutions that are not only secure but also manageable and performance-efficient. A key challenge in data encryption is key management—the secure generation, storage, distribution, and rotation of cryptographic keys. A lost key means lost data, so robust and user-friendly key management systems (KMS) are a major competitive differentiator. Furthermore, encryption can introduce performance overhead, so solutions that minimize the impact on application speed and user experience are highly valued. The vendors who can best balance ironclad security with operational simplicity and high performance will be best positioned to lead this vital and rapidly evolving market.

Explore Our Latest Trending Reports:

Proximity Access Control Market

Categories

Read More

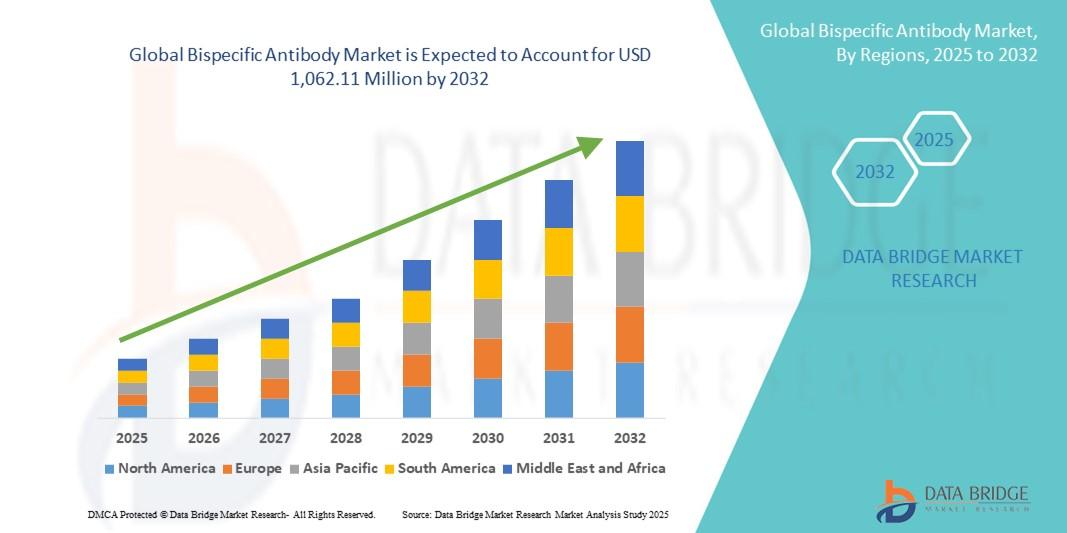

Discover the evolving dynamics of the bispecific antibody industry and its transformative impact on therapeutics. This report offers a detailed examination for informed business decisions. Get a full overview of market dynamics, forecasts, and trends. Download the complete Display Market report: https://www.databridgemarketresearch.com/reports/global-bispecific-antibody-market 1....

Executive Summary Animal Feed Market Size, Share, and Competitive Landscape CAGR Value The global Animal Feed market was valued at USD 196.92 billion in 2024 and is expected to reach USD 328.36 billion by 2032During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 6.60%, primarily driven by escalating global demand for animal protein To attain knowhow of...

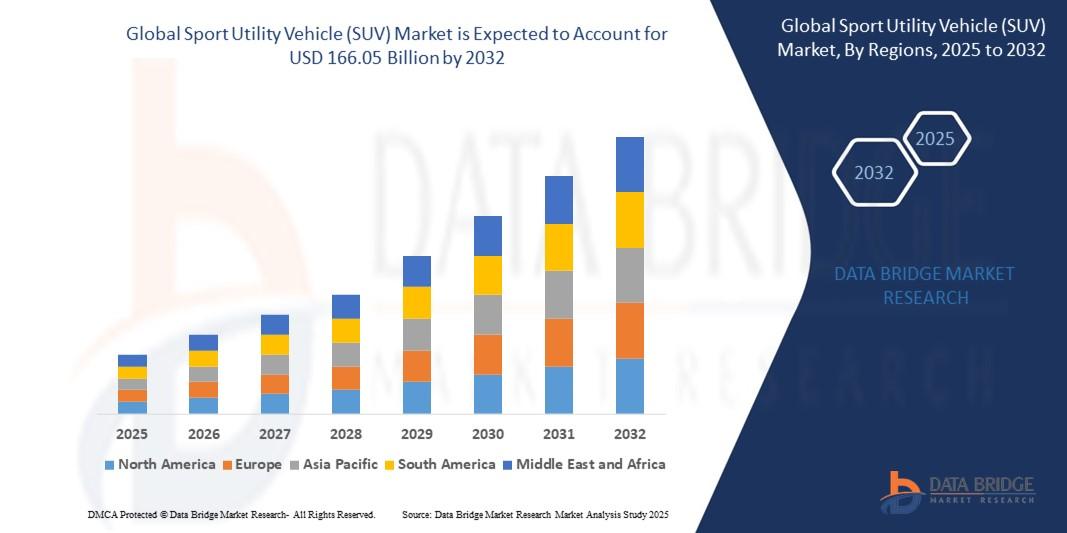

Introduction The Global Sport Utility Vehicle (SUV) Market has experienced remarkable growth over the past decade, establishing itself as one of the most dynamic segments within the automotive industry. SUVs, known for their versatility, comfort, and performance, have become increasingly popular among consumers worldwide. Rising urbanization, improved road infrastructure, growing...

"Regional Overview of Executive Summary Food Flavors Market by Size and Share CAGR Value Data Bridge Market Research analyzes that the global food flavors market is expected to reach the value of USD 29,484.11 million by 2030, at a CAGR of 6.1% during the forecast period. Natural Extracts account for the largest product type segment in the market due to their natural taste and health...

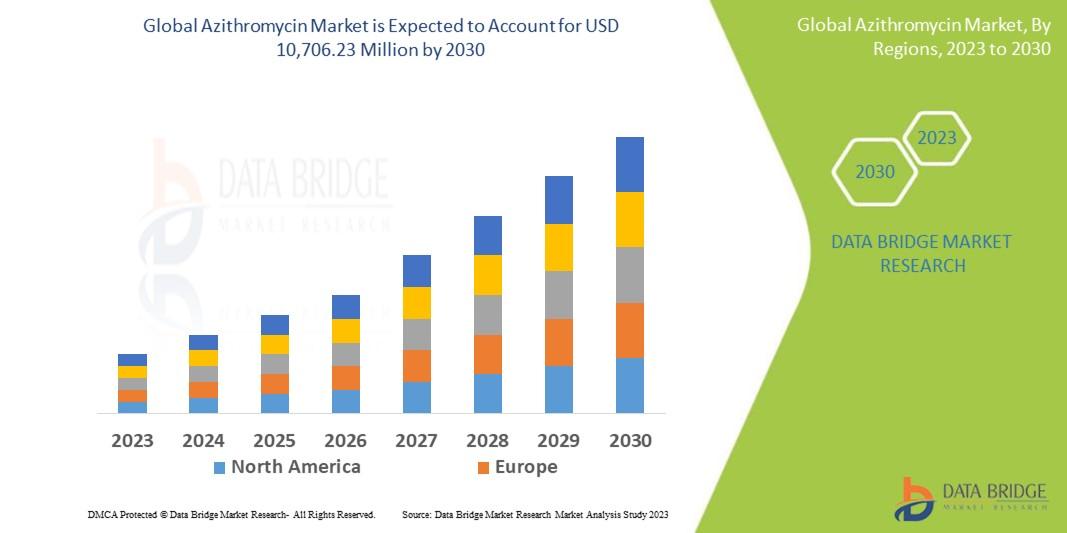

Rising demand for effective antibiotic therapies and increasing focus on accessible healthcare solutions are driving the expansion of the azithromycin market. This report provides a detailed outlook on industry dynamics, competitive strategies, and growth potential. Introduction Azithromycin is one of the most widely prescribed antibiotics, known for its efficacy in treating respiratory...